The following information has been updated for 2023 and 2024.

Here we go again! Now is a great time to do some year-end planning, especially for items that have an expiration date of December 31. There are several simple and smart actions you can take between now and the end of the year (and beyond).

RETIREMENT ACCOUNTS

By this time of the year, you should have a good idea of your total household income, as well as anticipated expenses (property tax, insurance dues, holiday gifts and donations, traveling plans, etc.). If your work situation is stable and household expenses are predictable, maximize retirement savings by looking at your cash flow situation and contributing to a retirement-savings vehicle – a 401(k) or other plan offered by your employer, or an individual retirement account (IRA).

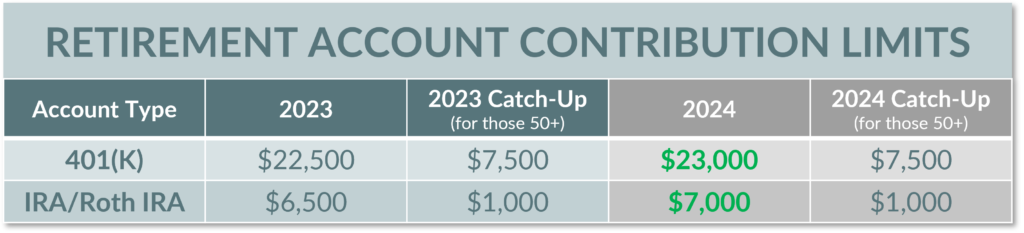

401(k)/403(b) Deferrals

Salary deferrals for 401(k) and 403(b) plans must go into your plan account by December 31st for them to count toward 2023. The contribution limit for 2023 is $22,500, while those over age 50 can contribute up to $30,000.

In 2024, the contribution limit will increase to $23,000 ($30,500 for participants 50 and older).

IRA Contributions

IRA contributions (regular and Roth) can be made up to the tax-filing day (April 15, 2024). The IRA contribution limit for 2023 is $6,500 ($7,500 for taxpayers 50 and older). See the table below for a summary.

In 2024, the contribution limit will increase to $7,000 ($8,000 for taxpayers 50 and older).

For those covered by a workplace retirement plan, the ability to make a deductible IRA contribution is subject to income limitations. Additionally, Roth IRA contributions are subject to income limitations and are not tax-deductible. Click these links for more information:

- 2023 IRA Contribution and Deduction Limits if You ARE Covered by a Retirement Plan at Work

- 2024 IRA Contribution and Deduction Limits if You ARE Covered by a Retirement Plan at Work

- 2023 Roth IRA Contribution Limits

- 2024 Roth IRA Contribution Limits

Roth Conversions

Weak markets provide opportune moments for Roth conversions. Read our blog post on Why You Should Seriously Consider Roth Conversions for more information.

HEALTHCARE

HEALTHCARE

Health Savings Accounts (HSAs)

Those covered by a high-deductible health plan can contribute tax-free into your health savings account (HSA) with no income phaseouts. The 2023 contribution limits (including any amount from your employer) are $3,850 for single taxpayers and $7,750 for families. Limits will increase to $4,150 (single) and $8,300 (family) in 2024. There is also a $1,000 catch-up for primary plan owners 55 and above.

Distributions used on qualified medical expenses are tax free. HSAs receive tax-free treatment on contributions, growth, and distributions, making them a top-notch savings vehicle. Better yet, both Schwab and Fidelity offer no-fee HSA brokerage accounts that allow you to invest the funds.

Flexible Spending Accounts (FSAs)

Flexible spending account (FSA) owners need to look at their account balances now. Generally, any unused funds are forfeited at the end of the year. If your FSA has a large balance, consider changing next year’s contribution amount. For ideas on how to spend down your FSA, read 42 Ways to Spend FSA Cash Before the Year-End Deadline or check out the FSA Store or Amazon’s list of eligible items. The federal government has made several changes to expand what FSA funds can be spent on during the pandemic.

A Dependent Care FSA provides additional flexibility for families with children in daycare or who have special needs.

Medicare

For those covered by Medicare, annual open enrollment (October 15 – December 7) allows you to review options and sign up for a new or different plan if desired. We have a local Medicare agent, BK Insurance, who can help members in Oregon and SW Washington. Give them a call if you are in need of coverage review.

GIFTING

Charitable Gifts

Here are some general charitable donation guidelines.

- For gifts under $500 – cash donations are effective for smaller gifts. Some of these don’t get acknowledged by the receiving charitable organizations. A good example is the Salvation Army red kettles outside a supermarket during the holiday season. Be sure to keep the receipts and a list of used items donated to Goodwill for tax purposes.

- For gifts $500 and above – we won’t stop you from giving cash if that is what you want to do. If your favorite charities can – and most do – accept securities such as stocks, you should take a look at your investment portfolio and see if it makes sense to give appreciated stocks. Giving appreciated stock is an effective way to give because you avoid paying taxes on capital gains while benefiting your favorite charities!

Qualified charitable distributions (QCDs), available only to IRA owners who are over age 70½, can reduce your required minimum distribution (RMD) amount while lowering taxable income. However, it’s important that you follow the rules in order for the donation not to be recognized as income. Also, if you take a normal distribution first and then a QCD, the donation will still be tax-free but the distribution you took first is considered taxable income. In other words, if your goal is to minimize a taxable RMD, be sure to process QCDs first.

Check out our blog post for more details and ideas on how make the most of your charitable donations.

Curious when you’ll have RMD? Take a look at our chart.

Personal Gifts

When it comes to personal gifts, sometimes it may be wise to give appreciated investments to family members rather than cash. Tax on long-term capital gains is omitted (0%) for married couples with taxable income up to $89,250 (singles $44,625). In other words, if you have family members with little or no income, they may be able to completely avoid capital gains tax on the appreciated assets. (Note: When gifting stocks, always gift stocks with long-term gains. Short-term gains are taxed as ordinary income and it’s a bad idea to gift stocks with losses.)

Annual gifts totaling $17,000 or less ($34,000 for married couples) per recipient do not have to be reported to the IRS and the recipient does not incur gift tax either. Keep in mind that you may gift more than $17,000 but must report it to the IRS.

WORKPLACE BENEFITS

Now is also an excellent time to re-evaluate your employment benefits and make adjustments if necessary. Many companies are currently accepting changes during their annual open enrollment period, which usually ends in mid-November. A few of the common benefits to review include:

- Group health plans – if you have changes in mind for the upcoming year, it’s wise to align the available benefits to fit your needs.

- Group life insurance – generally cheaper than individual policies and doesn’t require a medical exam.

- ESPP, or Employee Stock Purchase Plan – allows employees who work for a publicly-traded company to buy the company stock at a discount (typically 15%).

- Company discounts and wellness programs – many companies now offer benefits such as identity theft monitoring, legal services, and short-term disability insurance.

- Dependent Care FSA – allows you to use pre-tax dollars to pay for eligible dependent-care expenses, including daycare, preschool, and summer day camp. A spouse or a dependent who is incapable of self-care also qualifies.

Check out this WSJ article on How to Make the Most of Open Enrollment about why you should be thorough in reviewing your benefit options rather than making the quickest, simplest choice available.

If there are any items (whether covered in this blogpost or not) that you would like to discuss, do not hesitate to let us know.