In September, the Federal Reserve (Fed) voted to leave the federal funds rate unchanged. Numerous factors affected this decision, but perhaps the most important factor considered was the tenuous global economic situation. Raising U.S. rates at this critical juncture would have the effect of exacerbating currency and rate differentials across many countries.

Higher rates just aren’t justified when prices and growth remain constrained. In fact, on Tuesday, October 13, 2015, investors were content to purchase U.S. Treasury bills maturing in three months at a zero yield, only the second auction of those bills ever to deliver that result. A day later, one-month bills also sold at zero yields for the seventh straight time. That brings the total of zero-yield Treasuries to $1.17 trillion, or 3% of the total bill supply.[1]

However, this is not simply a U.S. phenomenon. Developed countries in general are moving dangerously close to a perpetual deflationary environment. In fact, in Europe, government debt maturing in two years in a number of countries, such as Germany, France and Finland, has been yielding below zero for months. In Switzerland, even government bonds due as far out as 2027 carry negative yields.[2] It seems that monetary-policy easing is pushing on a string.

Right now, world economies seem to be signaling for low rates into the foreseeable future. This is a positive development for debtors but not for savers. Capitalism works best with a healthy balance between debtors and lenders. The Fed has been anxious to stem the tide of easy money. Bad habits form when rates are low and leverage is cheap. The central bank had anticipated that they would be able to raise rates as needed. However, in my opinion, they did not anticipate the global strength of the dollar. As we raise rates, foreign money flows in to take advantage of these “risk-free” rates, which are high in comparison to other economic powerhouses like Germany and Japan and Switzerland. If economic indicators clearly signal the need to tighten, you can be sure that the Fed will act; and, over time, other economic zones will adjust accordingly to absorb higher U.S. rates. Several officials at the recent annual International Monetary Fund (IMF) annual meeting in Lima, Peru, urged the U.S. to act when necessary to keep the American economy strong, since that is in the best interest of global economic growth.[2]

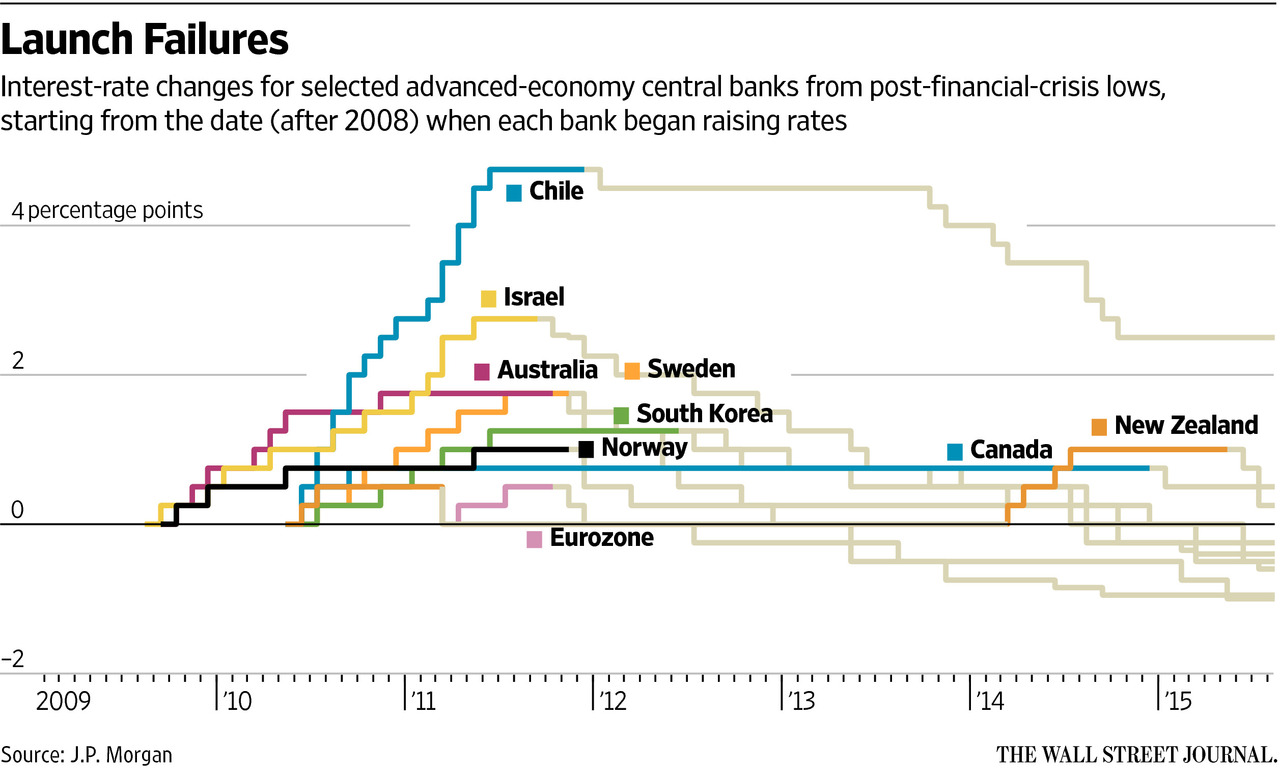

The Federal Reserve’s hesitancy is well founded because central banks in the euro zone, Sweden, Israel, Canada, South Korea, Australia, and Chile have tried to raise rates in recent years; only to reduce them again as their economies stumbled (see chart on next page).[3]

In fact, there have been about 700 rate cuts by central banks globally since the last Fed rate hike in 2006.[4]

Once again, the oft-foretold tightening has been postponed to a future date. As the Fed watches and waits, investors will have their patience tried as fixed income returns will be constrained. Summa continues to diversify the income holdings in your portfolio, in anticipation of the day that rates return to their long-term averages.

- http://on.wsj.com/1VTaxHo

- http://on.wsj.com/1LPqEQv

- http://on.wsj.com/1UQS2Z4

- Uncommon Sense. State Street Global Advisors. Michael Arone. October 2015.